ATR Regime Study [CHE] ATR Regime Study — ATR percentile regimes with clear bands, table and live label

Summary

This study classifies volatility into five regimes by converting ATR into a percentile rank over a rolling window, plotted on a standardized scale between zero and one hundred. Colored bands mark regime thresholds, while a compact table and an optional label report the current percentile and regime. The standardized scale makes symbols and timeframes easier to compare than raw ATR values. Implemented in Pine v6 as a separate pane (overlay set to false), it is a context tool to adapt tactics and risk handling to the prevailing volatility environment.

Motivation: Why this design?

Raw ATR varies with price scale and asset characteristics, which makes regime comparison inconsistent and leads to poor transfer of settings across symbols and timeframes. The core idea is to transform ATR into a percentile rank within a user-defined lookback, then map it into discrete regimes. This yields a stable, interpretable context signal that shifts slower than raw ATR while still responding to genuine volatility changes.

What’s different vs. standard approaches?

Reference baseline: Traditional ATR plots or ATR bands using fixed multipliers.

Architecture differences:

Percentile ranking of ATR within a rolling window.

Five discrete regimes with fixed thresholds at ninety, seventy, thirty, and ten.

Visual fills between thresholds plus a live table and a last-bar label.

Practical effect: You read a single normalized line between zero and one hundred with consistent thresholds. This improves cross-asset comparison and makes regime shifts obvious at a glance.

How it works (technical)

The script computes ATR over a configurable length, then converts that series to a percentile rank over a configurable number of bars. The percentile is naturally scaled and limited between zero and one hundred. That value is mapped to one of five regimes: above ninety (Extreme), between seventy and ninety (Elevated), between thirty and seventy (Normal), between ten and thirty (Calm), and below ten (Squeeze). Horizontal guide lines mark the thresholds, and fills shade the regions. A table is created once and updated on each bar to show regime definitions and highlight the current row. An optional label on the last bar displays the current percentile and regime. No higher-timeframe requests are used, so repaint risk is limited to normal live-bar fluctuation until the bar closes.

Parameter Guide

ATR length — Effect: Controls how fast ATR reacts to new ranges. Default: fourteen. Trade-offs/Tips: Increase to reduce noise in choppy markets; decrease to react faster during regime changes.

Percentile window (bars) — Effect: Number of bars used for the percentile ranking. Default: two hundred fifty-two. Trade-offs/Tips: Larger windows stabilize the percentile but slow adaptation after structural regime shifts; smaller windows adapt faster but may flip more often.

Table › Show — Effect: Toggles the regime overview table. Default: enabled. Trade-offs/Tips: Disable on constrained layouts to reduce visual clutter.

Table › Position — Effect: Anchors the table in a chart corner. Default: Top Right. Trade-offs/Tips: Choose a corner that avoids overlapping other panels or drawings.

Label › Show — Effect: Toggles a last-bar label with current percentile and regime. Default: enabled. Trade-offs/Tips: Useful for quick reads; disable if it obscures other annotations.

Reading & Interpretation

The white line shows ATR percentile between zero and one hundred. Crossing above seventy signals an elevated volatility environment; above ninety indicates event-driven extremes. Between thirty and seventy represents typical conditions. Between ten and thirty indicates calm conditions that often suit mean reversion. Below ten reflects compression, where breakout probability often increases. The colored bands visually reinforce these ranges. The table summarizes regime definitions and highlights the current state. The last-bar label mirrors the current percentile and regime for quick inspection.

Practical Workflows & Combinations

Trend following: Prefer continuation tactics when the percentile holds in the Normal or Elevated bands and structure confirms higher highs and higher lows. Consider wider stops and partial position sizing as percentile rises.

Mean reversion: Favor fades in Calm regimes within defined ranges; use structure filters and time-of-day constraints to avoid low-liquidity whipsaws.

Breakout preparation: Track compressions below ten; plan entries only with structure confirmation and risk caps, since compressions can persist.

Multi-asset/Multi-TF: Defaults travel well on daily charts. For intraday, reduce the percentile window to align with session dynamics. Combine with trend or market structure tools for confirmation.

Behavior, Constraints & Performance

Repaint/confirmation: The percentile updates during live bars and stabilizes on close; closed bars do not repaint.

security/HTF: Not used. If you add higher-timeframe aggregation externally, account for standard repaint caveats.

Resources: Declared maximum bars back is two thousand; limits for lines and labels are five hundred each. A short loop updates the table rows; arrays are used for table content only.

Known limits: Regime boundaries are fixed; assets with persistent volatility shifts may require window retuning. Low-liquidity periods and gaps can produce abrupt percentile changes. ATR is direction-agnostic and should be paired with trend or structure context.

Sensible Defaults & Quick Tuning

Start with ATR length fourteen and percentile window two hundred fifty-two on daily charts.

Too many flips: Increase ATR length or increase the percentile window.

Too sluggish: Decrease the percentile window or reduce ATR length.

Intraday noise: Keep ATR length moderate and reduce the window to a session-appropriate size; optionally hide the label to declutter.

Compressed markets: Maintain defaults but rely more on structure and volume filters before acting.

What this indicator is—and isn’t

This is a volatility regime context layer that standardizes ATR into interpretable regimes. It is not a complete trading system, not predictive, and not a stand-alone entry signal. Use it alongside structure analysis, confirmation tools, and disciplined risk management.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Best regards and happy trading

Chervolino

Cari dalam skrip untuk " TABLE "

RenKagi Fusion: Aura & SMA Clash IndicatorRenKagi Fusion: Aura & SMA Clash Indicator

Welcome to the RenKagi Fusion Indicator – a powerful, customizable tool that blends the strengths of Renko and Kagi charts to provide noise-filtered trend insights, enhanced with visual Aura effects and SMA (Simple Moving Average) crossover signals. Designed for traders seeking a unique edge in trend detection and reversal identification, this indicator combines traditional charting techniques with modern visualizations to help you navigate markets more effectively. Whether you're trading stocks, forex, or crypto, RenKagi Fusion offers a clean, actionable overview of market dynamics.

Key Features

RenKagi Line (Weighted Fusion of Renko and Kagi): The core of the indicator is the RenKagi line, a weighted average of Renko (brick-based trend filtering) and Kagi (reversal-focused line charts). Users can adjust the weight (default: 60% Renko, 40% Kagi) to prioritize stability or sensitivity. This fusion reduces market noise while highlighting key price movements.

Trend Scoring System: Calculates strength scores for Renko, Kagi, and RenKagi (capped at 20 points, converted to percentages). Scores increase with trend continuation and reset on reversals, giving a quantitative measure of momentum.

Aura Effects (Optional): Visual "glow" around lines based on score percentage – higher scores mean more opaque and thicker auras, adding a dynamic layer to trend visualization.

SMA Clash (Crossover Detection): Monitors daily SMA50, SMA100, and SMA200 for golden/death crosses (SMA50 crossing above/below longer SMAs) and RenKagi-SMA crossovers. These are displayed in a persistent info table for quick reference.

Customizable Visuals: Toggle lines, boxes, shapes, auras, and labels. Background coloring based on selected source (Renko, Kagi, or RenKagi) for intuitive trend bias.

Info Table: A configurable table (position and colors adjustable) summarizing scores, directions, cross states, brick size (with type), Kagi reversal (with type), and weights. No clutter – all in one place.

Alert Conditions: Built-in alerts for direction changes (Renko, Kagi, RenKagi), SMA crossovers, and golden/death crosses – perfect for real-time notifications.

How It Works

Renko Logic: Builds bricks based on user-selected type (Traditional fixed size, ATR dynamic, or Percentage). Scores build as trends persist, resetting on reversals.

Kagi Logic: Line reverses on thresholds (Traditional, ATR, or Percentage), scoring continuous moves.

RenKagi Calculation: Weighted average: (renkoPrice * renkoWeight + kagiLine * (100 - renkoWeight)) / 100. Score is a blend of individual scores.

SMA Integration: Daily timeframe SMAs for reliable long-term signals. Crossovers trigger alerts and update table states persistently until reversed.

Advantages for Traders

Noise Reduction: By fusing Renko's block structure with Kagi's reversal focus, it filters out minor fluctuations, helping identify strong trends early.

Versatility: Fully customizable – adjust weights, types, and visuals to fit any market or timeframe. Ideal for swing trading, trend following, or scalping.

Visual Clarity: Aura and background coloring provide at-a-glance insights, while the table consolidates data without overwhelming the chart.

Actionable Signals: Golden/Death crosses and direction changes offer clear entry/exit points, backed by alerts for timely execution.

Performance Optimization: Limits on lines/labels/boxes (500 each) ensure smooth operation on large datasets.

Usage Tips

Start with default settings for balanced performance.

Use in higher timeframes for trend confirmation or lower for intraday signals.

Combine with your favorite strategies – e.g., buy on RenKagi upward cross with SMA50 and golden cross confirmation.

Test on historical data to optimize weights and thresholds.

Note: This indicator is for educational and informational purposes only. Past performance is not indicative of future results. Always conduct your own analysis and use risk management. No financial advice is provided.

If you find this useful, please like, comment, or share your feedback!

Tzotchev Trend Measure [EdgeTools]Are you still measuring trend strength with moving averages? Here is a better variant at scientific level:

Tzotchev Trend Measure: A Statistical Approach to Trend Following

The Tzotchev Trend Measure represents a sophisticated advancement in quantitative trend analysis, moving beyond traditional moving average-based indicators toward a statistically rigorous framework for measuring trend strength. This indicator implements the methodology developed by Tzotchev et al. (2015) in their seminal J.P. Morgan research paper "Designing robust trend-following system: Behind the scenes of trend-following," which introduced a probabilistic approach to trend measurement that has since become a cornerstone of institutional trading strategies.

Mathematical Foundation and Statistical Theory

The core innovation of the Tzotchev Trend Measure lies in its transformation of price momentum into a probability-based metric through the application of statistical hypothesis testing principles. The indicator employs the fundamental formula ST = 2 × Φ(√T × r̄T / σ̂T) - 1, where ST represents the trend strength score bounded between -1 and +1, Φ(x) denotes the normal cumulative distribution function, T represents the lookback period in trading days, r̄T is the average logarithmic return over the specified period, and σ̂T represents the estimated daily return volatility.

This formulation transforms what is essentially a t-statistic into a probabilistic trend measure, testing the null hypothesis that the mean return equals zero against the alternative hypothesis of non-zero mean return. The use of logarithmic returns rather than simple returns provides several statistical advantages, including symmetry properties where log(P₁/P₀) = -log(P₀/P₁), additivity characteristics that allow for proper compounding analysis, and improved validity of normal distribution assumptions that underpin the statistical framework.

The implementation utilizes the Abramowitz and Stegun (1964) approximation for the normal cumulative distribution function, achieving accuracy within ±1.5 × 10⁻⁷ for all input values. This approximation employs Horner's method for polynomial evaluation to ensure numerical stability, particularly important when processing large datasets or extreme market conditions.

Comparative Analysis with Traditional Trend Measurement Methods

The Tzotchev Trend Measure demonstrates significant theoretical and empirical advantages over conventional trend analysis techniques. Traditional moving average-based systems, including simple moving averages (SMA), exponential moving averages (EMA), and their derivatives such as MACD, suffer from several fundamental limitations that the Tzotchev methodology addresses systematically.

Moving average systems exhibit inherent lag bias, as documented by Kaufman (2013) in "Trading Systems and Methods," where he demonstrates that moving averages inevitably lag price movements by approximately half their period length. This lag creates delayed signal generation that reduces profitability in trending markets and increases false signal frequency during consolidation periods. In contrast, the Tzotchev measure eliminates lag bias by directly analyzing the statistical properties of return distributions rather than smoothing price levels.

The volatility normalization inherent in the Tzotchev formula addresses a critical weakness in traditional momentum indicators. As shown by Bollinger (2001) in "Bollinger on Bollinger Bands," momentum oscillators like RSI and Stochastic fail to account for changing volatility regimes, leading to inconsistent signal interpretation across different market conditions. The Tzotchev measure's incorporation of return volatility in the denominator ensures that trend strength assessments remain consistent regardless of the underlying volatility environment.

Empirical studies by Hurst, Ooi, and Pedersen (2013) in "Demystifying Managed Futures" demonstrate that traditional trend-following indicators suffer from significant drawdowns during whipsaw markets, with Sharpe ratios frequently below 0.5 during challenging periods. The authors attribute these poor performance characteristics to the binary nature of most trend signals and their inability to quantify signal confidence. The Tzotchev measure addresses this limitation by providing continuous probability-based outputs that allow for more sophisticated risk management and position sizing strategies.

The statistical foundation of the Tzotchev approach provides superior robustness compared to technical indicators that lack theoretical grounding. Fama and French (1988) in "Permanent and Temporary Components of Stock Prices" established that price movements contain both permanent and temporary components, with traditional moving averages unable to distinguish between these elements effectively. The Tzotchev methodology's hypothesis testing framework specifically tests for the presence of permanent trend components while filtering out temporary noise, providing a more theoretically sound approach to trend identification.

Research by Moskowitz, Ooi, and Pedersen (2012) in "Time Series Momentum in the Cross Section of Asset Returns" found that traditional momentum indicators exhibit significant variation in effectiveness across asset classes and time periods. Their study of multiple asset classes over decades revealed that simple price-based momentum measures often fail to capture persistent trends in fixed income and commodity markets. The Tzotchev measure's normalization by volatility and its probabilistic interpretation provide consistent performance across diverse asset classes, as demonstrated in the original J.P. Morgan research.

Comparative performance studies conducted by AQR Capital Management (Asness, Moskowitz, and Pedersen, 2013) in "Value and Momentum Everywhere" show that volatility-adjusted momentum measures significantly outperform traditional price momentum across international equity, bond, commodity, and currency markets. The study documents Sharpe ratio improvements of 0.2 to 0.4 when incorporating volatility normalization, consistent with the theoretical advantages of the Tzotchev approach.

The regime detection capabilities of the Tzotchev measure provide additional advantages over binary trend classification systems. Research by Ang and Bekaert (2002) in "Regime Switches in Interest Rates" demonstrates that financial markets exhibit distinct regime characteristics that traditional indicators fail to capture adequately. The Tzotchev measure's five-tier classification system (Strong Bull, Weak Bull, Neutral, Weak Bear, Strong Bear) provides more nuanced market state identification than simple trend/no-trend binary systems.

Statistical testing by Jegadeesh and Titman (2001) in "Profitability of Momentum Strategies" revealed that traditional momentum indicators suffer from significant parameter instability, with optimal lookback periods varying substantially across market conditions and asset classes. The Tzotchev measure's statistical framework provides more stable parameter selection through its grounding in hypothesis testing theory, reducing the need for frequent parameter optimization that can lead to overfitting.

Advanced Noise Filtering and Market Regime Detection

A significant enhancement over the original Tzotchev methodology is the incorporation of a multi-factor noise filtering system designed to reduce false signals during sideways market conditions. The filtering mechanism employs four distinct approaches: adaptive thresholding based on current market regime strength, volatility-based filtering utilizing ATR percentile analysis, trend strength confirmation through momentum alignment, and a comprehensive multi-factor approach that combines all methodologies.

The adaptive filtering system analyzes market microstructure through price change relative to average true range, calculates volatility percentiles over rolling windows, and assesses trend alignment across multiple timeframes using exponential moving averages of varying periods. This approach addresses one of the primary limitations identified in traditional trend-following systems, namely their tendency to generate excessive false signals during periods of low volatility or sideways price action.

The regime detection component classifies market conditions into five distinct categories: Strong Bull (ST > 0.3), Weak Bull (0.1 < ST ≤ 0.3), Neutral (-0.1 ≤ ST ≤ 0.1), Weak Bear (-0.3 ≤ ST < -0.1), and Strong Bear (ST < -0.3). This classification system provides traders with clear, quantitative definitions of market regimes that can inform position sizing, risk management, and strategy selection decisions.

Professional Implementation and Trading Applications

The indicator incorporates three distinct trading profiles designed to accommodate different investment approaches and risk tolerances. The Conservative profile employs longer lookback periods (63 days), higher signal thresholds (0.2), and reduced filter sensitivity (0.5) to minimize false signals and focus on major trend changes. The Balanced profile utilizes standard academic parameters with moderate settings across all dimensions. The Aggressive profile implements shorter lookback periods (14 days), lower signal thresholds (-0.1), and increased filter sensitivity (1.5) to capture shorter-term trend movements.

Signal generation occurs through threshold crossover analysis, where long signals are generated when the trend measure crosses above the specified threshold and short signals when it crosses below. The implementation includes sophisticated signal confirmation mechanisms that consider trend alignment across multiple timeframes and momentum strength percentiles to reduce the likelihood of false breakouts.

The alert system provides real-time notifications for trend threshold crossovers, strong regime changes, and signal generation events, with configurable frequency controls to prevent notification spam. Alert messages are standardized to ensure consistency across different market conditions and timeframes.

Performance Optimization and Computational Efficiency

The implementation incorporates several performance optimization features designed to handle large datasets efficiently. The maximum bars back parameter allows users to control historical calculation depth, with default settings optimized for most trading applications while providing flexibility for extended historical analysis. The system includes automatic performance monitoring that generates warnings when computational limits are approached.

Error handling mechanisms protect against division by zero conditions, infinite values, and other numerical instabilities that can occur during extreme market conditions. The finite value checking system ensures data integrity throughout the calculation process, with fallback mechanisms that maintain indicator functionality even when encountering corrupted or missing price data.

Timeframe validation provides warnings when the indicator is applied to unsuitable timeframes, as the Tzotchev methodology was specifically designed for daily and higher timeframe analysis. This validation helps prevent misapplication of the indicator in contexts where its statistical assumptions may not hold.

Visual Design and User Interface

The indicator features eight professional color schemes designed for different trading environments and user preferences. The EdgeTools theme provides an institutional blue and steel color palette suitable for professional trading environments. The Gold theme offers warm colors optimized for commodities trading. The Behavioral theme incorporates psychology-based color contrasts that align with behavioral finance principles. The Quant theme provides neutral colors suitable for analytical applications.

Additional specialized themes include Ocean, Fire, Matrix, and Arctic variations, each optimized for specific visual preferences and trading contexts. All color schemes include automatic dark and light mode optimization to ensure optimal readability across different chart backgrounds and trading platforms.

The information table provides real-time display of key metrics including current trend measure value, market regime classification, signal strength, Z-score, average returns, volatility measures, filter threshold levels, and filter effectiveness percentages. This comprehensive dashboard allows traders to monitor all relevant indicator components simultaneously.

Theoretical Implications and Research Context

The Tzotchev Trend Measure addresses several theoretical limitations inherent in traditional technical analysis approaches. Unlike moving average-based systems that rely on price level comparisons, this methodology grounds trend analysis in statistical hypothesis testing, providing a more robust theoretical foundation for trading decisions.

The probabilistic interpretation of trend strength offers significant advantages over binary trend classification systems. Rather than simply indicating whether a trend exists, the measure quantifies the statistical confidence level associated with the trend assessment, allowing for more nuanced risk management and position sizing decisions.

The incorporation of volatility normalization addresses the well-documented problem of volatility clustering in financial time series, ensuring that trend strength assessments remain consistent across different market volatility regimes. This normalization is particularly important for portfolio management applications where consistent risk metrics across different assets and time periods are essential.

Practical Applications and Trading Strategy Integration

The Tzotchev Trend Measure can be effectively integrated into various trading strategies and portfolio management frameworks. For trend-following strategies, the indicator provides clear entry and exit signals with quantified confidence levels. For mean reversion strategies, extreme readings can signal potential turning points. For portfolio allocation, the regime classification system can inform dynamic asset allocation decisions.

The indicator's statistical foundation makes it particularly suitable for quantitative trading strategies where systematic, rules-based approaches are preferred over discretionary decision-making. The standardized output range facilitates easy integration with position sizing algorithms and risk management systems.

Risk management applications benefit from the indicator's ability to quantify trend strength and provide early warning signals of potential trend changes. The multi-timeframe analysis capability allows for the construction of robust risk management frameworks that consider both short-term tactical and long-term strategic market conditions.

Implementation Guide and Parameter Configuration

The practical application of the Tzotchev Trend Measure requires careful parameter configuration to optimize performance for specific trading objectives and market conditions. This section provides comprehensive guidance for parameter selection and indicator customization.

Core Calculation Parameters

The Lookback Period parameter controls the statistical window used for trend calculation and represents the most critical setting for the indicator. Default values range from 14 to 63 trading days, with shorter periods (14-21 days) providing more sensitive trend detection suitable for short-term trading strategies, while longer periods (42-63 days) offer more stable trend identification appropriate for position trading and long-term investment strategies. The parameter directly influences the statistical significance of trend measurements, with longer periods requiring stronger underlying trends to generate significant signals but providing greater reliability in trend identification.

The Price Source parameter determines which price series is used for return calculations. The default close price provides standard trend analysis, while alternative selections such as high-low midpoint ((high + low) / 2) can reduce noise in volatile markets, and volume-weighted average price (VWAP) offers superior trend identification in institutional trading environments where volume concentration matters significantly.

The Signal Threshold parameter establishes the minimum trend strength required for signal generation, with values ranging from -0.5 to 0.5. Conservative threshold settings (0.2 to 0.3) reduce false signals but may miss early trend opportunities, while aggressive settings (-0.1 to 0.1) provide earlier signal generation at the cost of increased false positive rates. The optimal threshold depends on the trader's risk tolerance and the volatility characteristics of the traded instrument.

Trading Profile Configuration

The Trading Profile system provides pre-configured parameter sets optimized for different trading approaches. The Conservative profile employs a 63-day lookback period with a 0.2 signal threshold and 0.5 noise sensitivity, designed for long-term position traders seeking high-probability trend signals with minimal false positives. The Balanced profile uses a 21-day lookback with 0.05 signal threshold and 1.0 noise sensitivity, suitable for swing traders requiring moderate signal frequency with acceptable noise levels. The Aggressive profile implements a 14-day lookback with -0.1 signal threshold and 1.5 noise sensitivity, optimized for day traders and scalpers requiring frequent signal generation despite higher noise levels.

Advanced Noise Filtering System

The noise filtering mechanism addresses the challenge of false signals during sideways market conditions through four distinct methodologies. The Adaptive filter adjusts thresholds based on current trend strength, increasing sensitivity during strong trending periods while raising thresholds during consolidation phases. The Volatility-based filter utilizes Average True Range (ATR) percentile analysis to suppress signals during abnormally volatile conditions that typically generate false trend indications.

The Trend Strength filter requires alignment between multiple momentum indicators before confirming signals, reducing the probability of false breakouts from consolidation patterns. The Multi-factor approach combines all filtering methodologies using weighted scoring to provide the most robust noise reduction while maintaining signal responsiveness during genuine trend initiations.

The Noise Sensitivity parameter controls the aggressiveness of the filtering system, with lower values (0.5-1.0) providing conservative filtering suitable for volatile instruments, while higher values (1.5-2.0) allow more signals through but may increase false positive rates during choppy market conditions.

Visual Customization and Display Options

The Color Scheme parameter offers eight professional visualization options designed for different analytical preferences and market conditions. The EdgeTools scheme provides high contrast visualization optimized for trend strength differentiation, while the Gold scheme offers warm tones suitable for commodity analysis. The Behavioral scheme uses psychological color associations to enhance decision-making speed, and the Quant scheme provides neutral colors appropriate for quantitative analysis environments.

The Ocean, Fire, Matrix, and Arctic schemes offer additional aesthetic options while maintaining analytical functionality. Each scheme includes optimized colors for both light and dark chart backgrounds, ensuring visibility across different trading platform configurations.

The Show Glow Effects parameter enhances plot visibility through multiple layered lines with progressive transparency, particularly useful when analyzing multiple timeframes simultaneously or when working with dense price data that might obscure trend signals.

Performance Optimization Settings

The Maximum Bars Back parameter controls the historical data depth available for calculations, with values ranging from 5,000 to 50,000 bars. Higher values enable analysis of longer-term trend patterns but may impact indicator loading speed on slower systems or when applied to multiple instruments simultaneously. The optimal setting depends on the intended analysis timeframe and available computational resources.

The Calculate on Every Tick parameter determines whether the indicator updates with every price change or only at bar close. Real-time calculation provides immediate signal updates suitable for scalping and day trading strategies, while bar-close calculation reduces computational overhead and eliminates signal flickering during bar formation, preferred for swing trading and position management applications.

Alert System Configuration

The Alert Frequency parameter controls notification generation, with options for all signals, bar close only, or once per bar. High-frequency trading strategies benefit from all signals mode, while position traders typically prefer bar close alerts to avoid premature position entries based on intrabar fluctuations.

The alert system generates four distinct notification types: Long Signal alerts when the trend measure crosses above the positive signal threshold, Short Signal alerts for negative threshold crossings, Bull Regime alerts when entering strong bullish conditions, and Bear Regime alerts for strong bearish regime identification.

Table Display and Information Management

The information table provides real-time statistical metrics including current trend value, regime classification, signal status, and filter effectiveness measurements. The table position can be customized for optimal screen real estate utilization, and individual metrics can be toggled based on analytical requirements.

The Language parameter supports both English and German display options for international users, while maintaining consistent calculation methodology regardless of display language selection.

Risk Management Integration

Effective risk management integration requires coordination between the trend measure signals and position sizing algorithms. Strong trend readings (above 0.5 or below -0.5) support larger position sizes due to higher probability of trend continuation, while neutral readings (between -0.2 and 0.2) suggest reduced position sizes or range-trading strategies.

The regime classification system provides additional risk management context, with Strong Bull and Strong Bear regimes supporting trend-following strategies, while Neutral regimes indicate potential for mean reversion approaches. The filter effectiveness metric helps traders assess current market conditions and adjust strategy parameters accordingly.

Timeframe Considerations and Multi-Timeframe Analysis

The indicator's effectiveness varies across different timeframes, with higher timeframes (daily, weekly) providing more reliable trend identification but slower signal generation, while lower timeframes (hourly, 15-minute) offer faster signals with increased noise levels. Multi-timeframe analysis combining trend alignment across multiple periods significantly improves signal quality and reduces false positive rates.

For optimal results, traders should consider trend alignment between the primary trading timeframe and at least one higher timeframe before entering positions. Divergences between timeframes often signal potential trend reversals or consolidation periods requiring strategy adjustment.

Conclusion

The Tzotchev Trend Measure represents a significant advancement in technical analysis methodology, combining rigorous statistical foundations with practical trading applications. Its implementation of the J.P. Morgan research methodology provides institutional-quality trend analysis capabilities previously available only to sophisticated quantitative trading firms.

The comprehensive parameter configuration options enable customization for diverse trading styles and market conditions, while the advanced noise filtering and regime detection capabilities provide superior signal quality compared to traditional trend-following indicators. Proper parameter selection and understanding of the indicator's statistical foundation are essential for achieving optimal trading results and effective risk management.

References

Abramowitz, M. and Stegun, I.A. (1964). Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables. Washington: National Bureau of Standards.

Ang, A. and Bekaert, G. (2002). Regime Switches in Interest Rates. Journal of Business and Economic Statistics, 20(2), 163-182.

Asness, C.S., Moskowitz, T.J., and Pedersen, L.H. (2013). Value and Momentum Everywhere. Journal of Finance, 68(3), 929-985.

Bollinger, J. (2001). Bollinger on Bollinger Bands. New York: McGraw-Hill.

Fama, E.F. and French, K.R. (1988). Permanent and Temporary Components of Stock Prices. Journal of Political Economy, 96(2), 246-273.

Hurst, B., Ooi, Y.H., and Pedersen, L.H. (2013). Demystifying Managed Futures. Journal of Investment Management, 11(3), 42-58.

Jegadeesh, N. and Titman, S. (2001). Profitability of Momentum Strategies: An Evaluation of Alternative Explanations. Journal of Finance, 56(2), 699-720.

Kaufman, P.J. (2013). Trading Systems and Methods. 5th Edition. Hoboken: John Wiley & Sons.

Moskowitz, T.J., Ooi, Y.H., and Pedersen, L.H. (2012). Time Series Momentum. Journal of Financial Economics, 104(2), 228-250.

Tzotchev, D., Lo, A.W., and Hasanhodzic, J. (2015). Designing robust trend-following system: Behind the scenes of trend-following. J.P. Morgan Quantitative Research, Asset Management Division.

Simplified Market ForecastSimplified Market Forecast Indicator

This indicator pairs nicely with the Contrarian 100 MA and can be located here:

Overview

The "Simplified Market Forecast" (SMF) indicator is a streamlined technical analysis tool designed for traders to identify potential buy and sell opportunities based on a momentum-based oscillator. By analyzing price movements relative to a defined lookback period, SMF generates clear buy and sell signals when the oscillator crosses customizable threshold levels. This indicator is versatile, suitable for various markets (e.g., forex, stocks, cryptocurrencies), and optimized for daily timeframes, though it can be adapted to other timeframes with proper testing. Its intuitive design and visual cues make it accessible for both novice and experienced traders.

How It Works

The SMF indicator calculates a momentum oscillator based on the price’s position within a specified range over a user-defined lookback period. It then smooths this value to reduce noise and plots the result as a line in a separate lower pane. Buy and sell signals are generated when the smoothed oscillator crosses above a user-defined buy level or below a user-defined sell level, respectively. These signals are visualized as triangles either on the main chart or in the lower pane, with a table displaying the current ticker and oscillator value for quick reference.

Key Components

Momentum Oscillator: The indicator measures the price’s position relative to the highest high and lowest low over a specified period, normalized to a 0–100 scale.

Signal Generation: Buy signals occur when the oscillator crosses above the buy level (default: 15), indicating potential oversold conditions. Sell signals occur when the oscillator crosses below the sell level (default: 85), suggesting potential overbought conditions.

Visual Aids: The indicator includes customizable horizontal lines for buy and sell levels, shaded zones for clarity, and a table showing the ticker and current oscillator value.

Mathematical Concepts

Oscillator Calculation: The indicator uses the following formula to compute the raw oscillator value:

c1I = close - lowest(low, medLen)

c2I = highest(high, medLen) - lowest(low, medLen)

fastK_I = (c1I / c2I) * 100

The result is smoothed using a 5-period Simple Moving Average (SMA) to produce the final oscillator value (inter).

Signal Logic:

A buy signal is triggered when the smoothed oscillator crosses above the buy level (ta.crossover(inter, buyLevel)).

A sell signal is triggered when the smoothed oscillator crosses below the sell level (ta.crossunder(inter, sellLevel)).

Entry and Exit Rules

Buy Signal (Blue Triangle): Triggered when the oscillator crosses above the buy level (default: 15), indicating a potential oversold condition and a buying opportunity. The signal appears as a blue triangle either below the price bar (if plotted on the main chart) or at the bottom of the lower pane.

Sell Signal (White Triangle): Triggered when the oscillator crosses below the sell level (default: 85), indicating a potential overbought condition and a selling opportunity. The signal appears as a white triangle either above the price bar (if plotted on the main chart) or at the top of the lower pane.

Exit Rules: Traders can exit positions when an opposite signal occurs (e.g., exit a buy on a sell signal) or based on additional technical analysis tools (e.g., support/resistance, trendlines). Always apply proper risk management.

Recommended Usage

The SMF indicator is optimized for the daily timeframe but can be adapted to other timeframes (e.g., 1H, 4H) with careful testing. It performs best in markets with clear momentum shifts, such as trending or range-bound conditions. Traders should:

Backtest the indicator on their chosen asset and timeframe to validate signal reliability.

Combine with other indicators (e.g., moving averages, support/resistance) or price action for confirmation.

Adjust the lookback period and buy/sell levels to suit market volatility and trading style.

Customization Options

Intermediate Length: Adjust the lookback period for the oscillator calculation (default: 31 bars).

Buy/Sell Levels: Customize the threshold levels for buy (default: 15) and sell (default: 85) signals.

Colors: Modify the colors of the oscillator line, buy/sell signals, and threshold lines.

Signal Display: Toggle whether signals appear on the main chart or in the lower pane.

Visual Aids: The indicator includes dotted horizontal lines at the buy (green) and sell (red) levels, with shaded zones between 0–buy level (green) and sell level–100 (red) for clarity.

Ticker Table: A table in the top-right corner displays the current ticker and oscillator value (in percentage), with customizable colors.

Why Use This Indicator?

The "Simplified Market Forecast" indicator provides a straightforward, momentum-based approach to identifying potential reversals in overbought or oversold markets. Its clear signals, customizable settings, and visual aids make it easy to integrate into various trading strategies. Whether you’re a swing trader or a day trader, SMF offers a reliable tool to enhance decision-making and improve market timing.

Tips for Users

Test the indicator thoroughly on your chosen asset and timeframe to optimize settings.

Use in conjunction with other technical tools for stronger trade confirmation.

Adjust the buy and sell levels based on market conditions (e.g., lower levels for less volatile markets).

Monitor the ticker table for real-time oscillator values to gauge market momentum.

Happy trading with the Simplified Market Forecast indicator!

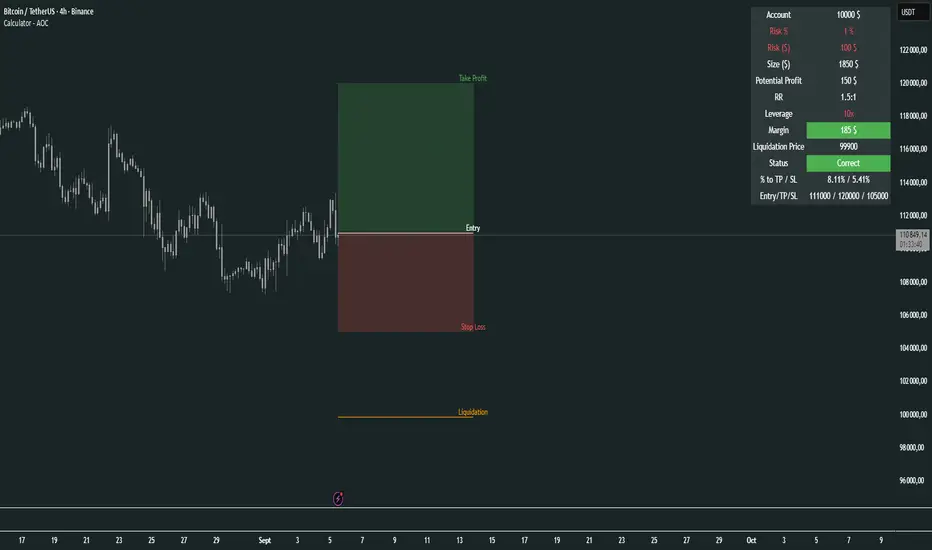

Calculator - AOC📊 Calculator - AOC Indicator 🚀

The Calculator - AOC indicator is a powerful and user-friendly tool designed for TradingView to help traders plan and visualize trades with precision. It calculates key trade metrics, displays entry, take-profit (TP), stop-loss (SL), and liquidation levels, and provides a clear overview of risk management and potential profits. Perfect for both novice and experienced traders! 💡

✨ Features

📈 Trade Planning: Input your Entry Price, Take Profit (TP), Stop Loss (SL), and Trade Direction (Long/Short) to visualize your trade setup on the chart.

💰 Risk Management: Set your Initial Capital and Risk per Trade (%) to calculate the optimal Position Size and Risk Amount for each trade.

⚖️ Leverage Support: Define your Leverage to compute the Required Margin and Liquidation Price, ensuring you stay aware of potential risks.

📊 Risk/Reward Ratio: Automatically calculates the Risk-to-Reward Ratio to evaluate trade profitability.

🎨 Visuals: Displays Entry, TP, SL, and Liquidation levels as lines and boxes on the chart, with customizable Line Width, Line Style, and Label Size.

✅ Trade Validation: Checks if your trade setup is valid (e.g., correct TP/SL placement) and highlights issues like potential liquidation risks with color-coded statuses (Correct ✅, Incorrect ❌, or Liquidation ⚠️).

📋 Summary Table: A clean, top-right table summarizes key metrics: Capital, Risk %, Risk Amount, Position Size, Potential Profit, Risk/Reward, Margin, Liquidation Price, Trade Status, and % to TP/SL.

🖌️ Customization: Adjust Line Extension (Bars) for how far lines extend, and choose from Solid, Dashed, or Dotted line styles for a personalized chart experience.

🛠️ How to Use

Add to Chart: Apply the indicator to your TradingView chart.

Configure Inputs:

Accountability: Set your Initial Capital and Risk per Trade (%).

Target: Enter Entry Price, TP, and SL prices.

Leverage: Specify your leverage (e.g., 10x).

Direction: Choose Long or Short.

Display Settings: Customize Line Width, Line Style, Label Size, and Line Extension.

Analyze: The indicator plots Entry, TP, SL, and Liquidation levels on the chart and displays a table with all trade metrics.

Validate: Check the Trade Status in the table to ensure your setup is valid or if adjustments are needed.

🎯 Why Use It?

Plan Smarter: Visualize your trade setup and understand your risk/reward profile instantly.

Stay Disciplined: Precise position sizing and risk calculations help you stick to your trading plan.

Avoid Mistakes: Clear validation warnings prevent costly errors like incorrect TP/SL placement or liquidation risks.

User-Friendly: Intuitive visuals and a summary table make trade analysis quick and easy.

📝 Notes

Ensure Entry, TP, and SL prices align with your trade direction to avoid "Incorrect" or "Liquidation" statuses.

The indicator updates dynamically on the latest bar, ensuring real-time visuals.

Best used with proper risk management to maximize trading success! 💪

Happy trading! 🚀📈

Yelober - Market Internal direction+ Key levelsYelober – Market Internals + Key Levels is a focused intraday trading tool that helps you spot high-probability price direction by anchoring decisions to structure that matters: yesterday’s RTH High/Low, today’s pre-market High/Low, and a fast Value Area/POC from the prior session. Paired with a compact market internals dashboard (NYSE/NASDAQ UVOL vs. DVOL ratios, VOLD slopes, TICK/TICKQ momentum, and optional VIX trend), it gives you a real-time read on breadth so you can choose which direction to trade, when to enter (breaks, retests, or fades at PMH/PML/VAH/VAL/POC), and how to plan exits as internals confirm or deteriorate. On top of these intraday decision benefits, it also allows traders—in a very subtle but powerful way—to keep an eye on the VIX and immediately recognize significant spikes or sharp decreases that should be factored in before entering a trade, or used as a quick signal to modify an existing position. In short: clear levels for the chart, live internals for the context, and a smarter, rules-based path to execution.

# Yelober – Market Internals + Key Levels

*A TradingView indicator for session key levels + real‑time market internals (NYSE/NASDAQ TICK, UVOL/DVOL/VOLD, and VIX).*

**Script name in Pine:** `Yelober - Market Internal direction+ Key levels` (Pine v6)

---

## 1) What this indicator does

**Purpose:** Help intraday traders quickly find high‑probability reaction zones and read market internals momentum without switching charts. It overlays yesterday/today’s **automatic price levels** on your active chart and shows a **market breadth table** that summarizes NYSE/NASDAQ buying pressure and TICK direction, with an optional VIX trend read.

### Key features at a glance

* **Automatic Price Levels (overlay on chart)**

* Yesterday’s High/Low of Day (**yHoD**, **yLoD**)

* Extended Hours High/Low (**yEHH**, **yEHL**) across yesterday AH + today pre‑market

* Today’s Pre‑Market High/Low (**PMH**, **PML**)

* Yesterday’s **Value Area High/Low** (**VAH/VAL**) and **Point of Control (POC)** computed from a volume profile of yesterday’s **regular session**

* Smart de‑duplication:

* Shows **only the higher** of (yEHH vs PMH) and **only the lower** of (yEHL vs PML) to avoid redundant bands

* **Market Breadth Table (on‑chart table)**

* **NYSE ratio** = UVOL/DVOL (signed) with **VOLD slope** from session open

* **NASDAQ ratio** = UVOLQ/DVOLQ (signed) with **VOLDQ slope** from session open

* **TICK** and **TICKQ**: live cumulative ratio and short‑term slope

* **VIX** (optional): current value + slope over a configurable lookback/timeframe

* Color‑coded trends with sensible thresholds and optional normalization

---

## 2) How to use it (trader workflow)

1. **Mark your reaction zones**

* Watch **yHoD/yLoD**, **PMH/PML**, and **VAH/VAL/POC** for first touches, break/retest, and failure tests.

* Expect increased responsiveness when multiple levels cluster (e.g., PMH ≈ VAH ≈ daily pivot).

2. **Read the breadth panel for context**

* **NYSE/NASDAQ ratio** (>1 = more up‑volume than down‑volume; <−1 = down‑dominant). Strong green across both favors long setups; red favors short setups.

* **VOLD slopes** (NYSE & NASDAQ): positive and accelerating → broadening participation; negative → persistent pressure.

* **TICK/TICKQ**: cumulative ratio and **slope arrows** (↗ / ↘ / →). Use the slope to gauge **near‑term thrust or fade**.

* **VIX slope**: rising VIX (red) often coincides with risk‑off; falling VIX (green) with risk‑on.

3. **Confluence = higher confidence**

* Example: Price reclaims **PMH** while **NYSE/NASDAQ ratios** print green and **TICK slopes** point ↗ — consider break‑and‑go; if VIX slope is ↘, that adds risk‑on confidence.

* Example: Price rejects **VAH** while **VOLD slopes** roll negative and VIX ↗ — consider fade/reversal.

4. **Risk management**

* Place stops just beyond key levels tested; if breadth flips, tighten or exit.

> **Timeframes:** Works best on 1–15m charts for intraday. Value Area is computed from **yesterday’s RTH**; choose a smaller calculation timeframe (e.g., 5–15m) for stable profiles.

---

## 3) Inputs & settings (what each option controls)

### Global Style

* **Enable all automatic price levels**: master toggle for yHoD/yLoD, yEHH/yEHL, PMH/PML, VAH/VAL/POC.

* **Line style/width**: applies to all drawn levels.

* **Label size/style** and **label color linking**: use the same color as the line or override with a global label color.

* **Maximum bars lookback**: how far the script scans to build yesterday metrics (performance‑sensitive).

### Value Area / Volume Profile

* **Enable Value Area calculations** *(on by default)*: computes yesterday’s **POC**, **VAH**, **VAL** from a simplified intraday volume profile built from yesterday’s **regular session bars**.

* **Max Volume Profile Points** *(default 50)*: lower values = faster; higher = more precise.

* **Value Area Calculation Timeframe** *(default 15)*: the security timeframe used when collecting yesterday’s highs/lows/volumes.

### Individual Level Toggles & Colors

* **yHoD / yLoD** (yesterday high/low)

* **yEHH / yEHL** (yesterday AH + today pre‑market extremes)

* **PMH / PML** (today pre‑market extremes)

* **VAH / VAL / POC** (yesterday RTH value area + point of control)

### Market Breadth Panel

* **Show NYSE / NASDAQ / VIX**: choose which series to display in the table.

* **Table Position / Size / Background Color**: UI placement and legibility.

* **Slope Averaging Periods** *(default 5)*: number of recent TICK/TICKQ ratio points used in slope calculation.

* **Candles for Rate** *(default 10)* & **Normalize Rate**: VIX slope calculation as % change between `now` and `n` candles ago; normalize divides by `n`.

* **VIX Timeframe**: optionally compute VIX on a higher TF (e.g., 15, 30, 60) for a smoother regime read.

* **Volume Normalization** (NYSE & NASDAQ): display VOLD slopes scaled to `tens/thousands/millions/10th millions` for readable magnitudes; color thresholds adapt to your choice.

---

## 4) Data sources & definitions

* **UVOL/VOLD (NYSE)** and **UVOLQ/DVOLQ/VOLDQ (NASDAQ)** via `request.security()`

* **Ratio** = `UVOL/DVOL` (signed; negative when down‑volume dominates)

* **VOLD slope** ≈ `(VOLD_now − VOLD_open) / bars_since_open`, then normalized per your setting

* **TICK/TICKQ**: cumulative sum of prints this session with **positives vs negatives ratio**, plus a simple linear regression **slope** of the last `N` ratio values

* **VIX**: value and slope across a user‑selected timeframe and lookback

* **Sessions (EST/EDT)**

* **Regular:** 09:30–16:00

* **Pre‑Market:** 04:00–09:30

* **After Hours:** 16:00–20:00

* **Extended‑hours extremes** combine **yesterday AH** + **today PM**

> **Note:** All session checks are done with TradingView’s `time(…,"America/New_York")` context. If your broker’s RTH differs (e.g., futures), adjust expectations accordingly.

---

## 5) How the algorithms work (plain English)

### A) Key Levels

* **Yesterday’s RTH High/Low**: scans yesterday’s bars within 09:30–16:00 and records the extremes + bar indices.

* **Extended Hours**: scans yesterday AH and today PM to get **yEHH/yEHL**. Script shows **either yEHH or PMH** (whichever is **higher**) and **either yEHL or PML** (whichever is **lower**) to avoid duplicate bands stacked together.

* **Value Area & POC (RTH only)**

* Build a coarse volume profile with `Max Volume Profile Points` buckets across the price range formed by yesterday’s RTH bars.

* Distribute each bar’s volume uniformly across the buckets it spans (fast approximation to keep Pine within execution limits).

* **POC** = bucket with max volume. **VA** expands from POC outward until **70%** of cumulative volume is enclosed → yields **VAH/VAL**.

### B) Market Breadth Table

* **NYSE/NASDAQ Ratio**: signed UVOL/DVOL with basic coloring.

* **VOLD Slopes**: from session open to current, normalized to human‑readable units; colors flip green/red based on thresholds that map to your normalization setting (e.g., ±2M for NYSE, ±3.5×10M for NASDAQ).

* **TICK/TICKQ Slope**: linear regression over the last `N` ratio points → **↗ / → / ↘** with the rounded slope value.

* **VIX Slope**: % change between now and `n` candles ago (optionally divided by `n`). Red when rising beyond threshold; green when falling.

---

## 6) Recommended presets

* **Stocks (liquid, intraday)**

* Value Area **ON**, `Max Volume Points` = **40–60**, **Timeframe** = **5–15**

* Breadth: show **NYSE & NASDAQ & VIX**, `Slope periods` = **5–8**, `Candles for rate` = **10–20**, **Normalize VIX** = **ON**

* **Index futures / very high‑volume symbols**

* If you see Pine timeouts, set `Max Volume Points` = **20–40** or temporarily **disable Value Area**.

* Keep breadth panel **ON** (it’s light). Consider **VIX timeframe = 15/30** for regime clarity.

---

## 7) Tips, edge cases & performance

* **Performance:** The volume profile is capped (`maxBarsToProcess ≤ 500` and bucketed) to keep it responsive. If you experience slowdowns, reduce `Max Volume Points`, `Maximum bars lookback`, or disable Value Area.

* **Redundant lines:** The script **intentionally suppresses** PMH/PML when yEHH/yEHL are more extreme, and vice‑versa.

* **Label visibility:** Use `Label style = none` if you only want clean lines and read values from the right‑end labels.

* **Futures/RTH differences:** Value Area is from **yesterday’s RTH** only; for 24h instruments the RTH period may not reflect overnight structure.

* **Session transitions:** PMH/PML tracking stops as soon as RTH starts; values persist as static levels for the session.

---

## 8) Known limitations

* Uses public TradingView symbols: `UVOL`, `VOLD`, `UVOLQ`, `DVOLQ`, `VOLDQ`, `TICK`, `TICKQ`, `VIX`. If your data plan or region limits any symbol, the corresponding table rows may show `na`.

* The VA/POC approximation assumes uniform distribution of each bar’s volume across its high–low. That’s fast but not a tick‑level profile.

* Works best on US equities with standard NY session; alternative sessions may need code changes.

---

## 9) Troubleshooting

* **“Script is too slow / timed out”** → Lower `Max Volume Points`, lower `Maximum bars lookback`, or toggle **OFF** `Enable Value Area calculations` for that instrument.

* **Missing breadth values** → Ensure the symbols above load on your account; try reloading chart or switching timeframes once.

* **Overlapping labels** → Set `Label style = none` or reduce label size.

---

## 10) Version / license / contribution

* **Version:** Initial public release (Pine v6).

* **Author:** © yelober

* **License:** Free for community use and enhancement. Please keep author credit.

* **Contributing:** Open PRs/ideas: presets, alert conditions, multi‑day VA composites, optional mid‑value (`(VAH+VAL)/2`), session filter for futures, and alertable state machine for breadth regime transitions.

---

## 11) Quick start (TL;DR)

1. Add the indicator and **keep default settings**.

2. Trade **reactions** at yHoD/yLoD/PMH/PML/VAH/VAL/POC.

3. Use the **breadth table**: look for **green ratios + ↗ slopes** (risk‑on) or **red ratios + ↘ slopes** (risk‑off). Check **VIX** slope for confirmation.

4. Manage risk around levels; when breadth flips against you, tighten or exit.

---

### Changelog (public)

* **v1.0:** First community release with automatic RTH levels, VA/POC approximation, breadth dashboard (NYSE/NASDAQ/TICK/TICKQ/VIX) with normalization and adaptive color thresholds.

Beta Zones [MMT]Beta Zones

Overview

The Beta Zones indicator is a multi-timeframe analysis tool designed to identify and visualize price ranges (zones) across different timeframes on a TradingView chart. It draws boxes to represent high and low price levels for each enabled timeframe, helping traders spot key support and resistance zones, track price movements, and assess market signals relative to these zones. The indicator is highly customizable, allowing users to toggle timeframes, adjust colors, and control historical visibility.

Features

Multi-Timeframe Support : Tracks up to five user-defined timeframes (default: 15m, 1H, 4H, 1D, 1W) to display price zones.

Dynamic Price Boxes : Draws boxes on the chart to represent the high and low prices for each timeframe, updating dynamically as new bars form.

Signal Indicators : Provides directional signals (▲, ▼, →) based on the previous close relative to the current box's top and bottom.

Customizable Display : Includes options to show or hide historical boxes, adjust box colors, and configure a summary table.

Summary Table : Displays a table with timeframe status, price range, and signal information for quick reference.

Settings

Timeframes

Enable/Disable : Toggle each timeframe (e.g., 15m, 1H, 4H, 1D, 1W) to display or hide its respective zones.

Timeframe Selection : Choose custom timeframes for each of the five slots.

Color Customization : Set unique fill and border colors for each timeframe's boxes (default colors: green, blue, orange, purple, red).

Display

Max Historical Boxes : Limit the number of historical boxes per timeframe (default: 1, max: 50).

Show History : Toggle visibility of historical boxes (default: false, showing only the latest box).

Min Box Height : Ensures boxes have a minimum height in ticks (default: 1.0, currently hardcoded).

Table

Show Table : Enable or disable the summary table (default: true).

Background Color : Customize the table's background color.

Header Color : Set the color for the table's header row.

Text Color : Adjust the text color for table content.

Table Columns

Timeframe : Displays the selected timeframe (e.g., 15m, 1H).

Color : Shows the color associated with the timeframe's boxes.

Status : Indicates if the timeframe is "Active" (valid and lower than the chart's timeframe), "Invalid" (enabled but not lower), or "Disabled".

Range : Shows the price range (high - low) of the current box.

Signal : Displays ▲ (price above box), ▼ (price below box), or → (price within box) based on the previous close.

How to Use

Add to Chart : Apply the indicator to your TradingView chart.

Configure Timeframes : Enable desired timeframes and adjust their settings (e.g., 15m, 1H) to match your trading strategy.

Analyze Zones : Use the boxes to identify key price levels for support, resistance, or breakout opportunities.

Monitor Signals : Check the table's "Signal" column to gauge price direction relative to each timeframe's zone.

Customize Appearance : Adjust colors and historical box visibility to suit your preferences.

Ideal For

Swing Traders : Identify key price zones across multiple timeframes for entry/exit points.

Day Traders : Monitor short-term price movements relative to higher timeframe zones.

Technical Analysts : Combine with other indicators to confirm support/resistance levels.

Weekly pecentage tracker by PRIVATE

Settings Picture below this link: 👇

i.ibb.co

What it is

A lightweight “Weekly % Tracker” overlay that lets you manually enter weekly performance (in percent) for XAUUSD + up to 10 FX pairs, then shows:

a small table panel with each enabled symbol and its % result

one TOTAL row (Sum / Average / Compounded across all enabled symbols)

an optional mini badge showing the % for a single selected symbol

Nothing is auto-calculated from price—you type the % yourself.

Key settings

Panel: show/hide, position, number of decimals, colors (background, text, green/red).

Total mode:

Sum – adds percentages

Average – mean of enabled rows

Compounded –

(

∏

(

1

+

𝑝

/

100

)

−

1

)

×

100

(∏(1+p/100)−1)×100

Symbols:

XAUUSD (toggle + label + % input)

10 FX pairs (each has On/Off, label text, % input). You can rename labels to any symbol text you want.

Mini badge: show/hide, position, and symbol to display.

How it works

Overlay indicator: overlay=true; just draws UI on the chart (no plots).

Arrays (syms, vals, ons) collect the row data in order: XAU first, then FX1…FX10.

Helpers:

posFrom() converts a position string (e.g., “Top Right”) into a position.* constant.

wp_col() picks green/red/neutral based on the sign of the %.

wp_round() rounds values to the selected decimals.

calc_total() computes the TOTAL with the chosen mode over enabled rows only.

Table creation logic:

Counts how many rows are enabled.

If none enabled or panel is off: the panel table is deleted, so no box/background is visible.

If enabled and on: the panel is (re)created at the chosen position.

On each last bar (barstate.islast), it clears the table to transparent (bgcolor=na) and then fills one row per enabled symbol, followed by a single TOTAL row.

Mini badge:

Always (re)created on position change.

Shows selected symbol’s % (or “-” if that symbol isn’t enabled or has no value).

Colors text green/red by sign.

Notes & limits

It’s manual input—the script doesn’t read trades or P/L from price.

You can rename each row’s label to match any symbol name you want.

When no rows are enabled, the panel disappears entirely (no empty background).

Designed to be light: only draws tables; no heavy plotting.

If you want the TOTAL row to be optional, or different color thresholds, or CSV-style export/import of the values, say the word and I’ll add it.

Mikula's Master 360° Square of 12Mikula’s Master 360° Square of 12

An educational W. D. Gann study indicator for price and time. Anchor a compact Square of 12 table to a start point you choose. Begin from a bar’s High or Low (or set a manual start price). From that anchor you can progress or regress the table to study how price steps through cycles in either direction.

What you’re looking at :

Zodiac rail (far left): the twelve signs.

Degree rail: 24 rows in 15° steps from 15° up to 360°/0°.

Transit rail and Natal rail: track one planet per rail. Each planet is placed at its current row (℞ shown when retrograde). As longitude advances, the planet climbs bottom → top, then wraps to the bottom at the next sign; during retrograde it steps downward.

Hover a planet’s cell to see a tooltip with its exact longitude and sign (e.g., 152.4° ♌︎). The linked price cell in the grid moves with the planet’s row so you can follow a planet’s path through the zodiac as a path through price.

Price grid (right): the 12×24 Square of 12. Each column is a cycle; cells are stepped price levels from your start price using your increment.

Bottom rail: shows the current square number and labels the twelve columns in that square.

How the square is read

The square always begins at the bottom left. Read each column bottom → top. At the top, return to the bottom of the next column and read up again. One square contains twelve cycles. Because the anchor can be a High or a Low, you can progress the table upward from the anchor or regress it downward while keeping the same bottom-to-top reading order.

Iterate Square (shifting)

Iterate Square shifts the entire 12×24 grid to the next set of twelve cycles.

Square 1 shows cycles 1–12; Square 2 shows 13–24; Square 3 shows 25–36, etc.

Visibility rules

Pivot cells are table-bound. If you shift the square beyond those prices, their highlights won’t appear in the table.

A/B levels and Transit/Natal planetary lines are chart overlays and can remain visible on the table as you shift the square.

Quick use

Choose an anchor (date/time + High/Low) or enable a manual start price .

Set the increment. If you anchored with a Low and want the table to step downward from there, use a negative value.

Optional: pick Transit and Natal planets (one per rail), toggle their plots, and hover their cells for longitude/sign.

Optional: turn on A/B levels to display repeating bands from the start price.

Optional: enable swing pivots to tint matching cells after the anchor.

Use Iterate Square to shift to later squares of twelve cycles.

Examples

These are exploratory examples to spark ideas:

Overview layout (zodiac & degree rails, Transit/Natal rails, price grid)

A-levels plotted, pivots tinted on the table, real-time price highlighted

Drawing angles from the anchor using price & time read from the table

Using a TradingView Gann box along the A-levels to study reactions

Attribution & originality

This script is an original implementation (no external code copied). Conceptual credit to Patrick Mikula, whose discussion of the Master 360° Square of 12 inspired this study’s presentation.

Further reading (neutral pointers)

Patrick Mikula, Gann’s Scientific Methods Unveiled, Vol. 2, “W. D. Gann’s Use of the Circle Chart.”

W. D. Gann’s Original Commodity Course (as provided by WDGAN.com).

No affiliation implied.

License CC BY-NC-SA 4.0 (non-commercial; please attribute @Javonnii and link the original).

Dependency AstroLib by @BarefootJoey

Disclaimer Educational use only; not financial advice.

Lot Size + Margin InfoThis indicator is designed to give Futures & Options traders instant access to lot size and estimated margin requirements for the instrument they are viewing — directly on their TradingView chart. It combines real-time symbol detection with a built-in, regularly updated margin lookup table (sourced from Kotak Securities’ published margin requirements), while also handling fallback logic for unknown or unsupported symbols.

---

### What It Does

* Automatically Detects the Instrument Type

Identifies whether the current chart’s symbol is a futures contract, option, or a cash/spot instrument.

* Shows Accurate Lot Size

For supported F\&O symbols, it fetches the correct lot size directly from exchange data.

For options, it retrieves the lot size from the option’s point value.

For cash/spot symbols with linked futures, it uses the futures lot size.

* Calculates Estimated Margin

* For futures: `Lot Size × Current Price × Margin%` (Margin% sourced from the internal lookup table).

* For options: `Lot Size × Current Price` (simple multiplication, as options margin ≈ premium cost).

* For unsupported or non-FnO symbols: Displays "No FnO".

* Fallback Margin Logic

If a symbol is missing from the margin lookup table, the script applies a user-defined default margin percentage and highlights the data in orange to indicate it’s using fallback values.

* Debug Mode for Transparency

A toggle to display the exact symbol string used for fetching lot size and margin, so traders can verify the data source.

---

### How It Works

1. Symbol Normalization

The script standardizes symbol names to match the margin table format (e.g., converting `"NIFTY1!"` to `"NIFTY"`).

2. Type-Based Handling

* Futures – Uses point value for lot size, applies specific margin % from the table.

* Options – Uses option point value for lot size, margin is simply premium × lot size.

* Cash Symbols with Linked Futures – Attempts to find and use the associated futures contract for lot/margin data.

* Unsupported Symbols – Displays `"No FnO"`.

3. Margin Table Integration

The margin % table is manually updated from a reliable broker’s margin sheet (Kotak Securities) — ensuring alignment with real trading conditions.

4. Customizable Display

* Position (Top Right / Bottom Left / Bottom Right)

* Table background color, text color, font size, border width

* Editable label text for lot size and margin display

* Toggleable lot size and margin sections

---

### How to Use

1. Add the Indicator to Your Chart – Works on any NSE Futures, Options, or Cash symbol with linked F\&O.

2. Configure Display Settings – Choose whether to show lot size, margin, or both, and place the info table where you prefer.

3. Adjust Fallback Margin % – If you trade less common contracts, set your default margin % to reflect your broker’s requirement.

4. Enable Debug Mode (Optional) – To see the exact symbol source the script is using.

---

### Best For

* Intraday & Positional F\&O Traders who need instant clarity on lot size and margin before entering trades.

* Options Sellers & Buyers who want quick cost estimates.

* Traders Switching Symbols Quickly — saves time by removing the need to check the broker’s margin sheet manually.

---

💡 Pro Tip: Since margin requirements can change, keep the script updated whenever your broker revises margin data. This version’s margin table is updated as of 13-08-2025.

Volume Delta Pressure Tracker by GSK-VIZAG-AP-INDIA📢 Title:

Volume Delta Pressure Tracker by GSK-VIZAG-AP-INDIA

📝 Short Description (for script title box):

Real-time volume pressure tracker with estimated Buy/Sell volumes and Delta visualization in an Indian-friendly format (K, L, Cr).

📃 Full Description

🔍 Overview:

This indicator estimates buy and sell volumes using candle structure (OHLC) and displays a real-time delta table for the last N candles. It provides traders with a quick view of volume imbalance (pressure) — often indicating strength behind price moves.

📊 Features:

📈 Buy/Sell Volume Estimation using the candle’s OHLC and Volume.

⚖️ Delta Calculation (Buy Vol - Sell Vol) to detect pressure zones.

📅 Time-stamped Table displaying:

Time (HH:MM)

Buy Volume (Green)

Sell Volume (Red)

Delta (Color-coded)

🔢 Indian Number Format (K = Thousands, L = Lakhs, Cr = Crores).

🧠 Fully auto-calculated — no need for tick-by-tick bid/ask feed.

📍 Neatly placed bottom-right table, customizable number of rows.

🛠️ Inputs:

Show Table: Toggle the table on/off

Number of Bars to Show: Choose how many recent candles to include (5–50)

🎯 Use Cases:

Identify hidden buyer/seller strength

Detect volume absorption or exhaustion

✅ Compatibility:

Works on any timeframe

Ideal for intraday instruments like NIFTY, BANKNIFTY, etc.

Ideal for volume-based strategy confirmation.

🖋️ Developed by:

GSK-VIZAG-AP-INDIA

Awesome Indicator# Moving Average Ribbon with ADR% - Complete Trading Indicator

## Overview

The **Moving Average Ribbon with ADR%** is a comprehensive technical analysis indicator that combines multiple analytical tools to provide traders with a complete picture of price trends, volatility, relative performance, and position sizing guidance. This multi-faceted indicator is designed for both swing and positional traders looking for data-driven entry and exit signals.

## Key Components

### 1. Moving Average Ribbon System

- **4 Customizable Moving Averages** with default periods: 13, 21, 55, and 189

- **Multiple MA Types**: SMA, EMA, SMMA (RMA), WMA, VWMA

- **Color-coded visualization** for easy trend identification

- **Flexible configuration** allowing users to modify periods, types, and colors

### 2. Average Daily Range Percentage (ADR%)

- Calculates the average daily volatility as a percentage

- Uses a 20-period simple moving average of (High/Low - 1) * 100

- Helps traders understand the stock's typical daily movement range

- Essential for position sizing and stop-loss placement

### 3. Volume Analysis (Up/Down Ratio)

- Analyzes volume distribution over the last 55 periods

- Calculates the ratio of volume on up days vs down days

- Provides insight into buying vs selling pressure

- Values > 1 indicate more buying volume, < 1 indicate more selling volume

### 4. Absolute Relative Strength (ARS)

- **Dual timeframe analysis** with customizable reference points

- **High ARS**: Performance relative to benchmark from a high reference point (default: Sep 27, 2024)

- **Low ARS**: Performance relative to benchmark from a low reference point (default: Apr 7, 2025)

- Uses NSE:NIFTY as default comparison symbol

- Color-coded display: Green for outperformance, Red for underperformance

### 5. Relative Performance Table

- **5 timeframes**: 1 Week, 1 Month, 3 Months, 6 Months, 1 Year

- Shows stock performance **relative to benchmark index**

- Formula: (Stock Return - Index Return) for each period

- **Color coding**:

- Lime: >5% outperformance

- Yellow: -5% to +5% relative performance

- Red: <-5% underperformance

### 6. Dynamic Position Allocation System

- **6-factor scoring system** based on price vs EMAs (21, 55, 189)

- Evaluates:

- Price above/below each EMA

- EMA alignment (21>55, 55>189, 21>189)

- **Allocation recommendations**:

- 100% allocation: Score = 6 (all bullish signals)

- 75% allocation: Score = 4

- 50% allocation: Score = 2

- 25% allocation: Score = 0

- 0% allocation: Score = -2, -4, -6 (bearish signals)

## Display Tables

### Performance Table (Top Right)

Shows relative performance vs benchmark across multiple timeframes with intuitive color coding for quick assessment.

### Metrics Table (Bottom Right)

Displays key statistics:

- **ADR%**: Average Daily Range percentage

- **U/D**: Up/Down volume ratio

- **Allocation%**: Recommended position size

- **High ARS%**: Relative strength from high reference

- **Low ARS%**: Relative strength from low reference

## How to Use This Indicator

### For Trend Analysis

1. **Moving Average Ribbon**: Look for price above ascending MAs for bullish trends

2. **MA Alignment**: Bullish when shorter MAs are above longer MAs

3. **Color coordination**: Use consistent color scheme for quick visual analysis

### For Entry/Exit Timing

1. **Performance Table**: Enter when showing consistent outperformance across timeframes

2. **Volume Analysis**: Confirm entries with U/D ratio > 1.5 for strong buying

3. **ARS Values**: Look for positive ARS readings for relative strength confirmation

### For Position Sizing

1. **Allocation System**: Use the recommended allocation percentage

2. **ADR% Consideration**: Adjust position size based on volatility

3. **Risk Management**: Lower allocation in high ADR% stocks

### For Risk Management

1. **ADR% for Stop Loss**: Set stops at 1-2x ADR% below entry

2. **Relative Performance**: Reduce positions when consistently underperforming

3. **Volume Confirmation**: Be cautious when U/D ratio deteriorates

## Best Practices

### Timeframe Recommendations

- **Intraday**: Use lower MA periods (5, 13, 21, 55)

- **Swing Trading**: Default settings work well (13, 21, 55, 189)

- **Position Trading**: Consider higher periods (21, 50, 100, 200)

### Market Conditions

- **Trending Markets**: Focus on MA alignment and relative performance

- **Sideways Markets**: Rely more on ADR% for range trading

- **Volatile Markets**: Reduce allocation percentage regardless of signals

### Customization Tips

1. Adjust reference dates for ARS calculation based on significant market events

2. Change comparison symbol to sector-specific indices for better relative analysis

3. Modify MA periods based on your trading style and market characteristics

## Technical Specifications

- **Version**: Pine Script v6

- **Overlay**: Yes (plots on price chart)

- **Real-time Updates**: Yes